Healthcare Concepts We Keep Getting Expensively Wrong

Episode 2: Growth — The Number That Lies in Plain Sight

The companion series to “Healthcare Metrics That Look Great and Still Don’t Fix Anything.” The metrics series is about numbers that lie. This one is about ideas that do the same thing — just without a dashboard to hide behind.

(Previously: Episode 1 — Scale: The Pin Factory Problem. And: Scale — The Thing You Can’t Put in a Playbook, Part II

There is a sentence that has appeared in more healthcare board presentations, investor decks, and acquisition post-mortems than any other sentence in the industry:

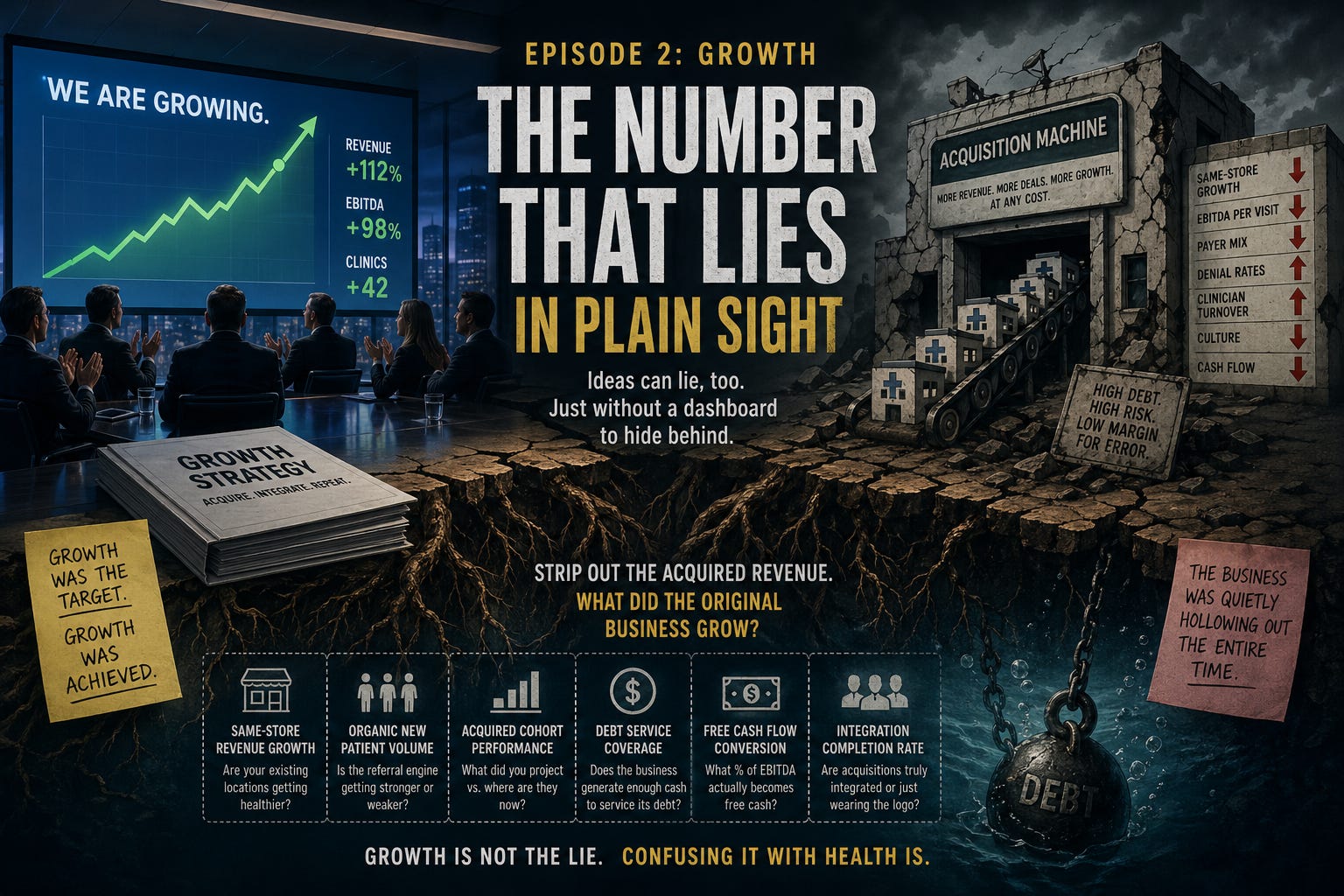

“We are growing.”

It is said with confidence. It is often accompanied by a chart pointing up and to the right. It is almost never followed by the question that actually matters:

Growing how? And growing what?

The Origin of the Confusion

“Growth” entered healthcare operator vocabulary the same way most management concepts do — from the financial world, where it actually means something specific: net new revenue generated by the underlying business through organic activity. New customers, expanded relationships, more volume from existing locations. The market equivalent of a patient getting better.

What happened in healthcare platforms — especially through the PE-backed roll-up era — is that “growth” quietly became a container for two fundamentally different things: organic growth (the business is actually healthier and busier than it was) and inorganic growth (we bought another clinic’s revenue and added it to ours). Both show up on the same top-line number. Both get presented to the board as “growth.” Only one of them tells you whether the underlying business is working.

This is Goodhart’s Law — Extremal variant. When growth becomes the target, operators pursue it to the logical extreme: an acquisition machine that manufactures headline revenue regardless of what the underlying business is actually doing. The metric grows. The business may not be. And by the time you can tell the difference, the debt is already there.

What the Top Line Hides

Here is a scenario that has played out across every healthcare specialty in the last decade. See if it sounds familiar.

A platform acquires 12 clinics in 18 months. Revenue doubles. The board celebrates. The unqualified CEO amends their CV for active search conversations. The investment deck shows a hockey stick. The recap process begins, and growth is exhibit A.

Meanwhile: same-clinic visit volume at the original locations is flat or declining — and even where visits are up, that number is being conflated with actual growth. More visits do not equal more cash. A platform can report rising visit volume while reimbursement rates are declining, payer mix is worsening, culture becomes toxic, founders and those that are integral to the business are run off or quit, denial rates are climbing, and EBITDA per visit is shrinking. Presenting visit growth as business growth is a half-truth at best and misdirection at worst — the word “growth” doing work it hasn’t earned. The acquired clinics are underperforming their underwriting assumptions. The organic new patient rate is dropping. Clinician turnover is rising. And the debt service on the acquisitions is consuming the free cash flow that would have gone to investing in the original locations.

But the top line is growing.

Growth was the target. Growth was achieved. The business was quietly hollowing out the entire time.

I documented this pattern in my PPM series on The Operator, specifically about the post-PE acquisition movie that replays on an 18-month cycle: “Eighteen months later, revenue is trending toward the exit while leadership reports ‘growth’ — growth that is entirely acquired, never benchmarked against organic performance or what the acquisition itself was supposed to deliver. The movie ends the same way every time. Somehow nobody in the room has seen it before.”

Nobody in the room asks the right question because the right question is inconvenient. The right question is: strip out the acquired revenue. What did the original business grow?

The Bodies Are Real

This isn’t a theoretical concern about incentive misalignment. I’ve documented the wreckage in detail on multiple PE-backed healthcare platforms and the retail giants who collectively deployed $20 billion into healthcare roll-ups and largely got the same result — in a prior post on The Operator covering the five dysfunctions of PE-backed healthcare platforms. The pattern is consistent enough to have its own genre.

The short version: every one of them was reporting growth until the moment they weren’t. The top line went up. The debt service didn’t.

If you want the full case files, that post is worth the read. Here, the more useful question is why the metric reliably produces this outcome — and what to track instead.

The Free-Money Accelerant

To be fair to the platforms that failed: they were operating in an environment that actively rewarded the wrong behavior for more than a decade.

When the federal funds rate sat near zero for twelve years, debt was essentially free. A healthcare platform could carry leverage ratios that would have been disqualifying in any rational capital environment and still service the debt comfortably. The business model didn’t have to be great. It had to be adequate. The financing did the rest. Between 2019 and 2021, large PT platforms were closing at 14x–16x EBITDA. Dental DSO multiples were similarly detached from operational reality. Orthopedics groups were acquired at numbers that only penciled if rates stayed near zero forever and growth was linear into infinity.

Nobody in the room asked what happened if either assumption changed. Both did. Simultaneously.

The fastest rate increase in 40 years, starting in 2022, meant that the same platform — same revenue, same margins, same clinicians — was now structurally underwater on its debt. Nothing operationally changed. The macro did. The acquisitions that had been “growth” were now anchors.

The free-money era was a decade-long audition that let everyone skip the part where the business actually had to work. That audition is over.

Why the Concept Warps the Behavior

Here is the Goodhart mechanism, clearly stated:

When top-line growth becomes the primary performance metric — reported to the board, included in management comp, used to justify the recap valuation — the organization optimizes for it. The fastest way to grow revenue in healthcare services is to acquire it. Organic growth is slow, requires investment in existing locations, and produces messy unit economics conversations. Inorganic growth is fast, photogenic, and generates immediate headline revenue.

So the acquisition machine starts. Each deal adds to the top line. The integration — the hard, unglamorous work of actually making the acquired practice run on shared systems, shared culture, shared clinical standards — gets de-prioritized because it doesn’t generate a headline number. The existing clinicians watch the culture get diluted with each successive deal. The same-store economics erode. The engagement scores drop before the revenue does.

And the board slide still says: we are growing.

This is the Extremal variant at work. The concept, pursued to its logical extreme, eventually destroys the thing it was supposed to measure. Growth pursued without constraint became the mechanism of the collapse.

Same-Store Growth: The Number That Tells the Truth

There is a single number that cuts through almost all of the noise in healthcare platform performance reporting: same-store revenue growth — revenue change at locations that existed in both the current and prior periods, stripped of any acquired or divested revenue.

Same-store growth is not glamorous. It doesn’t generate headlines. It can’t be goosed by a deal. It is simply the question: are the practices you already had getting healthier?

If same-store growth is positive, the underlying business is working. If it’s flat, you’re treading water. If it’s negative — which it often is in platforms that have been aggressively acquiring — you are buying revenue to cover the fact that your existing business is declining. And the cost of that acquisition is sitting on your balance sheet, accruing interest, waiting for the moment when the market stops being generous.

What to measure alongside or instead of top-line growth:

Same-store revenue growth (existing locations, year-over-year, acquisitions stripped out entirely)

Organic new patient volume trend — is the referral engine getting stronger or weaker at current locations?

Acquired cohort performance vs. underwriting — what did you project when you bought this practice, and where is it now? Tracked systematically, not reported selectively.

Debt service coverage ratio — unglamorous, essential. Does the business generate enough cash to service its debt? Not the EBITDA. The cash.

Free cash flow conversion — what percentage of reported EBITDA actually becomes free cash? A platform with deteriorating collections, worsening payer mix, and rising denial rates can show stable EBITDA for 12–18 months while quietly destroying its cash position. The board sees EBITDA. The business feels the cash.

Integration completion rate — what percentage of acquired practices are actually running on shared systems and shared culture, vs. sharing a logo and a debt obligation?

The Closing Argument

The platforms still standing after the post-2022 reckoning are, almost without exception, the ones that prioritized organic performance over acquisition volume — and were honest with themselves about the difference.

As I noted in the PPM series, the management candidates worth hiring are specifically those who can show you same-store performance through the hard years: recessionary periods or the post-COVID period when labor costs spiked, supply chains broke, reimbursement got cut, and clinician shortages became the new normal. Anyone can look like an operator in a free-money environment where acquisitions inflate the top line and cheap debt covers the rest. The question is what they grew when they couldn’t buy their way to it.

Growth is a legitimate business objective. It becomes a Goodhart problem the moment it stops being a consequence of operational health and starts being the thing the operational decisions are optimized to produce.

If your growth strategy is designed to generate a top-line number rather than a stronger underlying business, you’re not growing. You’re borrowing the appearance of growth from your future self — and your future self has a debt payment due.

larry

Thanks for reading The Operator. If you enjoyed this post (or even if you didn’t but appreciate someone finally saying it out loud), subscribe to receive new posts and support my work. Let’s keep the conversation — and the accountability — going.

This is the natural follow to the Scale piece, and the pharmacy parallel is even cleaner. The PBM industry has been running the exact same play.

The Big 3 PBMs report consolidated revenue growth that mixes organic (winning new plan sponsor business on the merits) and structurally inorganic (members routed through PBM ownership via the bundled carrier-PBM-pharmacy stack their parent company controls). UnitedHealth's most recent quarterly disclosure shows intercompany eliminations growing 256% over the last decade while overall revenue grew 151%. That delta is exactly the metric you describe: growth that did not require a better product, just an acquired channel.

Your same-store equivalent in pharmacy benefits is per-member, per-employer-plan trend year over year, stripped of bundling effects. Net cost trend, denial rates, pass-through capture, pharmacy network experience. Most of those numbers are not reported back to the plan sponsor in a way that makes the Goodhart problem visible. The board slide says "managed PMPM growth." The plan watching its own claims data sees something different.

The free-money era part of your argument applies here too, with a different accelerant. Low cost of capital let PE-backed PBM-adjacent companies (specialty pharmacy, PA tech, formulary tech) over-acquire on the same logic. The post-2022 reckoning is now sorting out which of those layers actually had unit economics and which were debt service in a wig.

Looking forward to the rest of the series.

What a mess. So obvious the end game. All at the expense of the humans that trusted that healthcare received would be in their interests.

Now what? Have the dentists, therapists and doctors (and all their patients) try again?